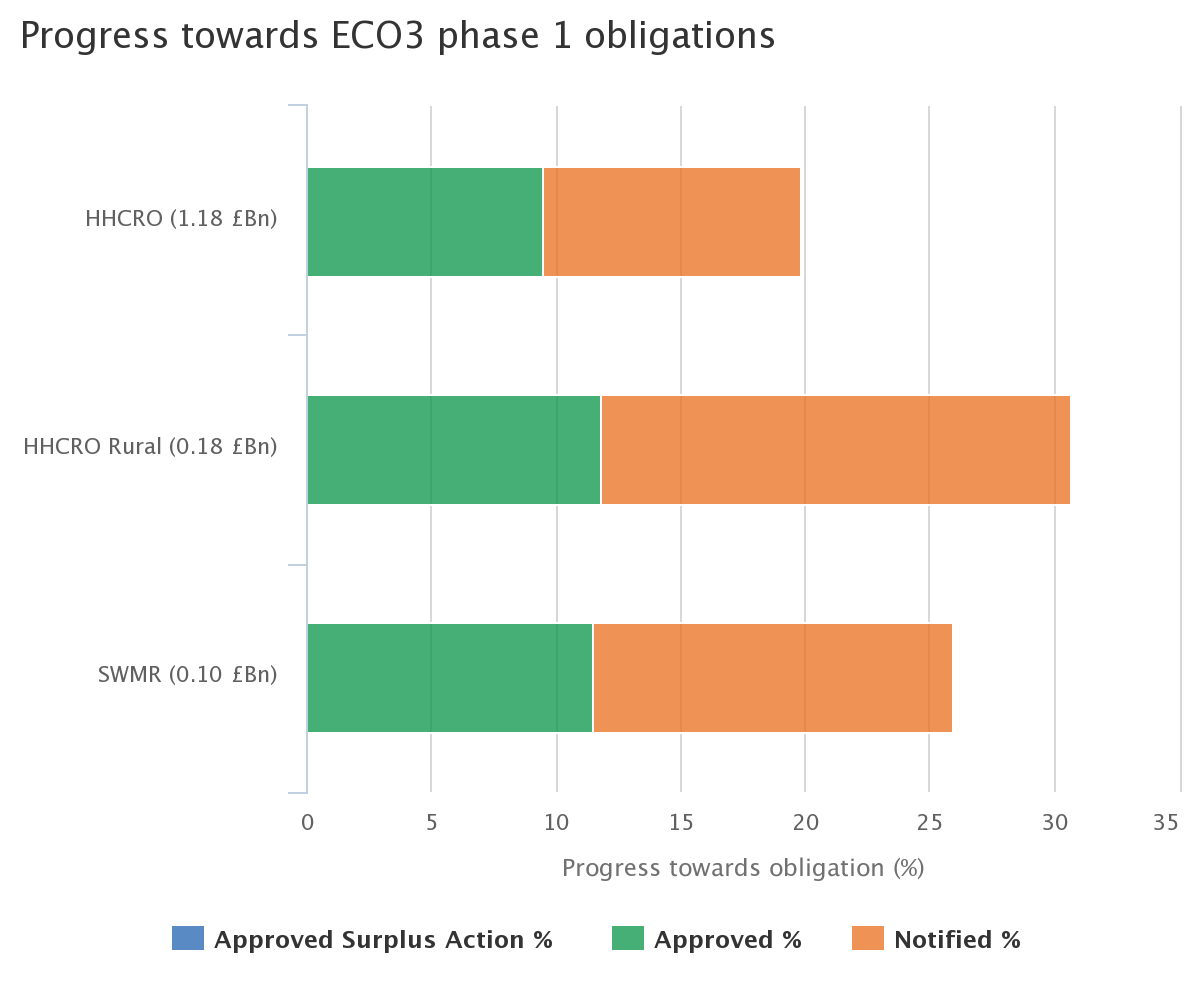

Unlike its predecessor schemes, uptake of ECO3 is extremely slow and worrying. Following chart from Ofgem’s ECO3 progress report (published in April 2019) shows that only about 20% progress was made against the phase 1.

Is ECO dead already? As long as ECO Legislation is in effect the obligations have to be met. The current scenario however, looks bleak and there are no immediate hopes for improvement. All you hear about in ECO is how small installers are shutting down, how some installers are agreeing to deliver at unsustainable rates, and how some ECO2 boilers might have been replaced in ECO3 on the ground that they would have outlived their lifetime of 4 years as per the revised lifetime of boilers in ECO3.

Here is my analysis of what’s going wrong with ECO at the moment. Resourcematics provide Compliance and reporting services to suppliers, managing agents and installers. The analysis presented here is the gist of our discussions with various stakeholders. We would welcome your comments and views on this.

Uncertainty

The scheme started in October 2018 amidst lack of clarity about delivery rules. The first version of delivery guidance was published around Christmas, and ever since then the rules and associated compliance documents keep changing. The same is happening to the deemed scores; scores corrected, partial fill cavity scores introduced (that too without consultation!), and there are still unresolved queries around scores for some measures like park homes.

Delivery costs

Removal of CERO has made customer identification a challenge. Most qualifying customers struggle to contribute towards to cost of installation (remember, they are already fuel poor or at the risk of fuel poverty). Besides, there is a looming cost on installers of implementing PAS2035. Restrictions on promoting heating measures, officially undermining the importance of solid wall insulation and restricting the blending of RHI funding with ECO on certain renewable technologies also has a direct impact of the uptake of these measures and their delivery costs. The release of PAS2035 will only make things difficult on the ground. No one will be able to measure the impact of PAS2035 if ECO3 delivery doesn’t pick up.

Rock bottom prices

The current funding rates are miles away from what BEIS had predicted in their ECO3 impact assessment (anyone surprised though?). Energy price caps are often cited as a reason for reduced spending on ECO, but we also cannot rule out the impact of the uncapped carry over from ECO2 HHCRO and up to 20% carry over from CERO on the slow progress of ECO3. More on this can be understood once Ofgem publishes progress reports on approved surplus actions.

What’s next?

Implementation of PAS 2035 would require legislative amendments in ECO3 Order, hence there should be a consultation on its way soon after the publication of PAS2035. Consultations provide an opportunity for the stakeholders to present the reality and their views to the Government. A realistic policy will certainly give the much-needed push to the delivery and brings things back to an equilibrium. If you have any suggestions, we would love to hear from you.